January 2026 Monthly Review

"What Am I Going To Do?"

LJohnson@fcbanking.com

412-208-7687

Connect on LinkedIn

A Look Back

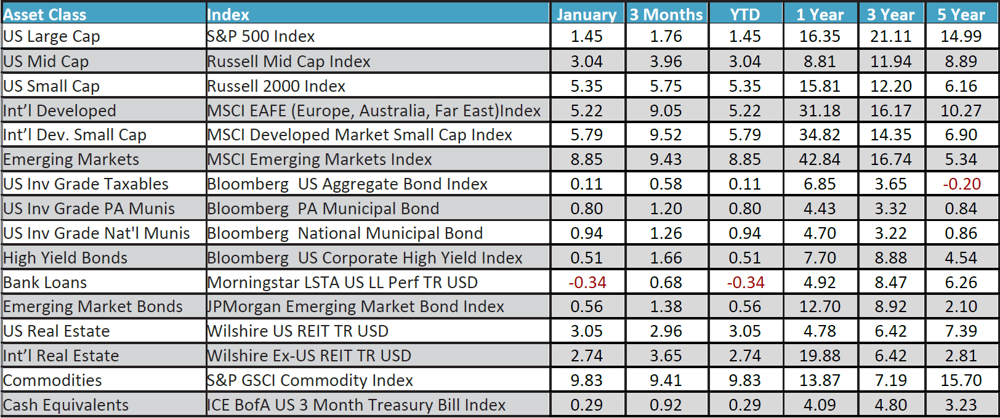

The above title is from the 2023 song recorded by country icon, Chris Stapleton. The song about heartbreak was co-written by female country star, Miranda Lambert. It ponders the aftermath of a broken relationship. The two had written other songs together through the years and sang this together for the first time live in 2024 as part of his “All-American Road Show.” I heard it recently, and it reminded me of current market conditions. After three years of outstanding stock market performance, many are wondering what to do. Most major indices are sitting at or near all-time highs after posting returns more than double the long-term average in each of the last three calendar years. That, coupled with some economic and geo-political uncertainty brings a heightened sense of anxiety to many. With that backdrop, the first month of 2026 saw stock markets around the globe continuing their march onward and upward. The large-cap S&P 500 was the laggard in January with a 1.45% return. Small-cap domestic stocks did much better with a 5.35% increase, and international stocks fared the best. Emerging market equities really started the year off with a robust 8.85% return. That normally would not be a bad number for an entire year! Core bonds eked out a small gain of .11% for the month, and almost 7% over the last year. Commodities, fueled by an uptick in energy prices and precious metals, surged nearly 10% in January.

The latest economic releases here in the U.S. showed an economy that was slowing, but importantly still plodding ahead, as evidenced by the 4.4% third quarter GDP increase. The employment situation showed 50,000 jobs added in December and the unemployment rate remained stable at 4.4%, still a low number historically. Inflation remains sticky, as the most recent report pegged year-over-year CPI at 2.7%. Finally, although buoyed by the top 10% of earners, consumers are still spending. We have written in the past about the increasing bifurcation of overall spending…the haves and the have-nots…and how that is not the most ideal situation for a truly healthy and sustainable economy. The hard-working middle class needs to be a consistent contributor for longer-lasting, continued growth, as the Fed works toward their ultimate goal of around 2% yearly inflation.

A Look Ahead

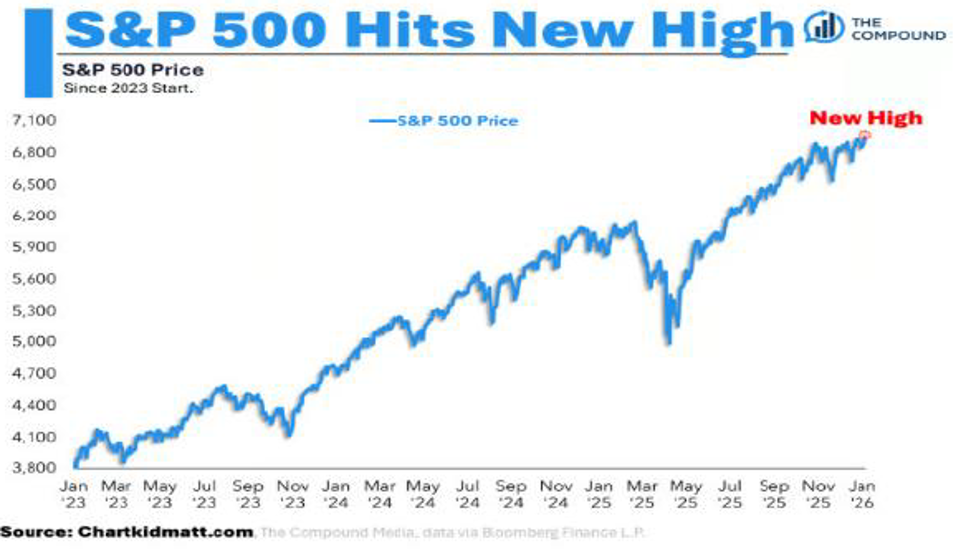

I know the chart above is small because of limited space, but I believe it’s important to include it for perspective. It depicts the S&P 500 price move from the beginning of 2023. There’s a quick and significant dip in April of 2025 after the initial Tariff plan was released, but then a sustained rally into year-end…and now early 2026 with new high after new high. In fact, there were 43 new all-time highs posted in 2025. Investors would have missed a nice little rally if they waited after the first high…Historically, the numbers suggest that there is little difference in forward returns no matter when you invest. We currently have a slight overweight to stocks in general and emerging markets specifically. We believe core bond returns will be more muted this year than last as we navigate a declining short-term rate environment and a more static middle part of the yield curve. That’s where we are and what we are going to do…